Can PayPal stock recover and double in value by 2026 after reaching its 52-week low?

PAYPAL STOCK

Key Points

PayPal remains a global leader in digital payments with diversified revenue streams and a trusted brand, despite recent stock declines and increased competition.

The company faces challenges such as slow revenue growth, leadership transitions, and intensified competition from major fintech rivals like Apple Pay and Google Pay.

PayPal's strong fundamentals, continued profitability, and opportunities for international expansion position it for potential recovery and growth by 2026 if it can address current weaknesses.

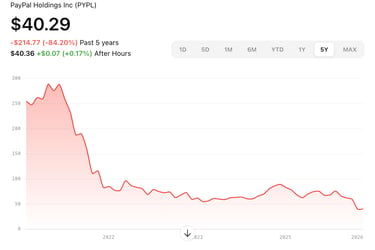

Last week, PayPal (NASDAQ: PYPL) reached a new 52-week low, falling below $40. The stock is now at prices last seen in 2017, which is troubling for long-term investors. After reaching a record high of $307.82 in July 2021, PayPal has lost more than 85% of its value, raising concerns among shareholders.

A sudden CEO change, disappointing earnings, and weak 2026 guidance exacerbated Wall Street's concerns. Some value investors see this drop as an opportunity, whereas others view it as a value trap due to leadership changes and rising competition.

“The following SWOT analysis evaluates the key internal and external factors impacting the Company.”

Global leader in digital Payment

PayPal is one of the most trusted digital payment brands, with about 438 million active accounts. Despite intense competition, PayPal is increasing its profit margins by leveraging a dual-sided ecosystem that links merchants and consumers.

PayPal has diversified revenue streams that generate billions of dollars in revenue. PayPal Checkout enables consumers to pay directly by selecting PayPal on a merchant's website or app. The second is unbranded checkout, called Braintree. Companies like Uber, Airbnb, and DoorDash use this feature so consumers can pay without a PayPal login. The third is Venmo, which allows users to send and receive money directly without a bank transfer.

PayPal offers chargeback protection and advanced fraud protection tools to merchants. This results in fast transaction approvals and increases overall payment volume and fee revenue.

Leadership Transition and Slow Revenue Growth

PayPal faces several key weaknesses. Growth has slowed significantly compared to 2020-2021. PayPal derives most of its revenue from its core direct checkout business, which has grown extremely slowly, raising long-term investor concerns.

PayPal's revenue is heavily dependent on E-Commerce Businesses. Unlike Apple or Google Pay, PayPal doesn't control hardware or operating Systems. Tariffs and uncertainty are putting margin pressure, compressing margins in the near term.

Technological Disruptions & Intense Competition

PayPal faces intense competition from major fintech companies such as Apple Pay, Google Pay, Block, and Stripe. This strong rivalry could lower prices, reduce market share, and limit future growth.

New real-time payment systems and alternative payment fintech may further disrupt PayPal Business. Many investors favour high-growth companies, yet they regard PayPal as a mature fintech firm despite its financial performance having stabilized.

Growth opportunities for PayPal Holdings

As Internet access, Technology adoption, and e-commerce activity continue to expand across many parts of Africa and Southeast Asia, PayPal has a significant opportunity to capture market share through merchant partnerships and cross-border transaction volume.

Even PayPal's stock has been hit hard over the last 5 years, but the company’s fundamentals have improved significantly. The stock is trading at a P/E of 7.45 and yields 1.39%, indicating it is undervalued. The company has positive free cash flow exceeding USD 5.5 billion and is buying back shares aggressively.

Image by Mohamed Hassan from Pixabay

Disclaimer: This post is for educational and informational purposes only and does not provide financial, investment, legal, or tax advice. www.vandhdaan.com is not a licensed financial advisor. Please consult a qualified professional before making financial decisions based on this content.

Read More ....

Contact

Newsletter

admin@vandhdaan.com

© 2026. All rights reserved.